.png)

Cash App Borrow fees and interest rate lawsuit investigation

Shamis & Gentile P.A., one of the nation's premier class action law firms with a primary focus in arbitration cases,, is investigating potential claims against Cash App related to its “Borrow” loan feature and other consumer-facing practices.

If someone has been charged high fees, faced aggressive repayment tactics or experienced other problems with Cash App, they may be eligible for compensation through arbitration.

What is Cash App?

Cash App is a mobile financial services app operated by Block Inc., the company formerly known as Square. Launched in 2013 as a simple peer-to-peer payment tool, Cash App allows users to send and receive money digitally, often functioning as an alternative to traditional bank transfers.

Users can receive direct deposits such as paychecks, spend with a branded Cash Card, buy stocks in small dollar amounts and trade Bitcoin. Cash App also offers a short-term lending feature commonly referred to as “Borrow,” which allows eligible users to take out small loans directly through the app.

Cash App reports tens of millions of monthly active customers and operates across the United States and other markets.

Why is Cash App being investigated?

The investigation focuses on concerns that Cash App’s short-term “Borrow” loans and related repayment practices may be unfair, deceptive or otherwise unlawful under consumer protection laws.

Publicly available information and consumer reports indicate that:

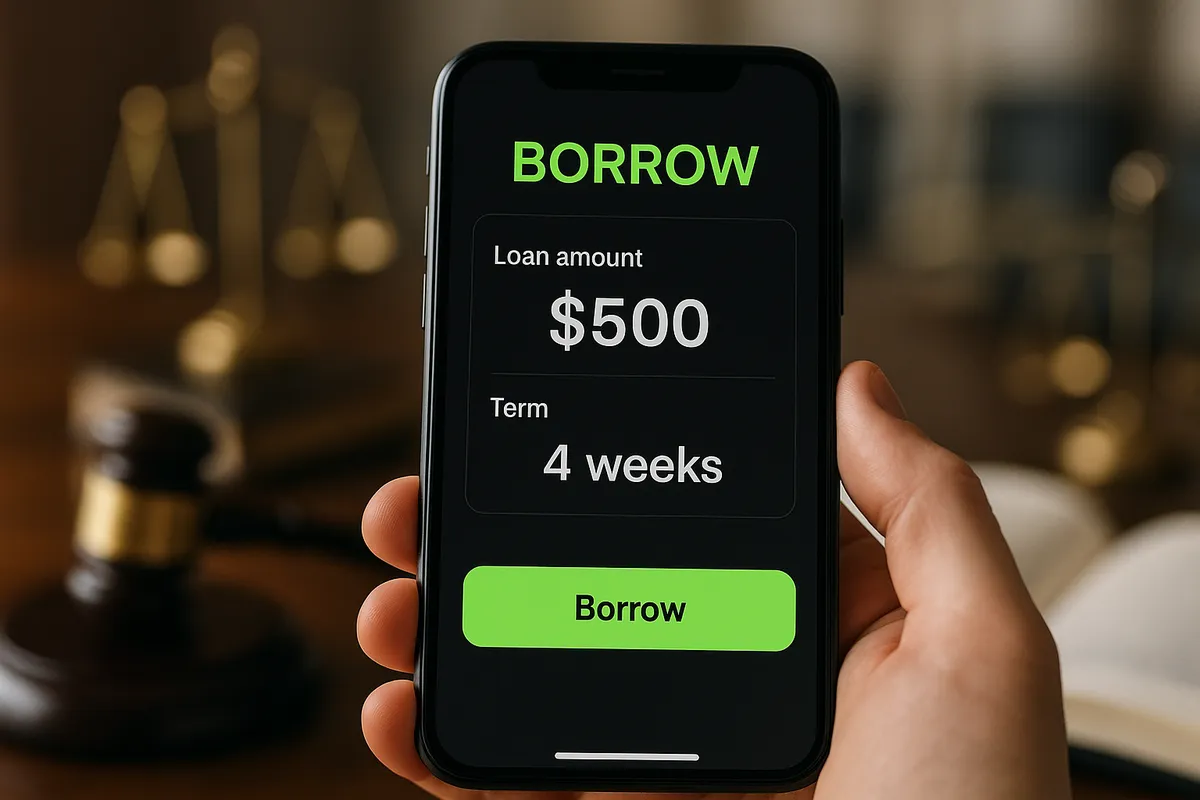

- Cash App “Borrow” loans typically range from about $20 up to a few hundred dollars, often around a $200 maximum, with repayment usually due within about four weeks

- Instead of traditional interest, Cash App charges a flat fee (reported around 5 percent of the loan amount) and may add an additional weekly fee (reported around 1.25 percent per week) if the loan is not repaid on time

- When converted to an annual percentage rate, or APR, these fees can translate into extremely high effective interest rates, sometimes estimated in the range of 60 percent to 200 percent or more

Consumers have raised several concerns about how this may play out in real life:

- Potentially predatory cost structure: Small, short-term loans with high effective APRs can trap borrowers in cycles of debt, especially those already facing financial hardship

- Insufficient disclosure or understanding of true cost: While Cash App may show the total repayment amount, many borrowers may not realize how expensive the loan is when viewed as an APR or compared with other credit options

- Automatic repayment practices: Cash App can automatically pull repayment from a user’s Cash App balance, which may be funded by paychecks or other deposits. This can leave borrowers without money for rent, food or other essentials and may trigger overdrafts or other downstream financial harm

- Repeat borrowing cycles: Because eligibility is based largely on app usage rather than a full review of ability to repay, some users may be repeatedly offered new loans even when they are struggling to pay off prior ones

A team of lawyers is investigating whether, taken together, these practices may violate state or federal consumer protection laws, usury laws, unfair and deceptive acts and practices (UDAP) statutes, or other legal protections designed to prevent abusive lending and collection behavior.

Your Rights and Next Steps

People who used Cash App’s “Borrow” feature or experienced aggressive repayment or fee practices may have important legal rights, even if they signed Cash App’s user agreement or arbitration clause.

Depending on the facts, potential legal claims being investigated may include:

- Unfair or deceptive practices: If Cash App failed to clearly and prominently disclose the true cost of borrowing, or if the design of the app encouraged users to take loans without fully understanding the risks

- Predatory or usurious lending: If the effective interest rates and fee structures violate state interest rate caps or other lending laws

- Improper or abusive collection practices: If automatic withdrawals, timing of debits or repeated attempts to collect caused avoidable harm such as overdraft fees, account closures or inability to pay basic living expenses

- Breach of contract or breach of the duty of good faith: If Cash App did not follow its own stated terms or applied them in a way that was unfair or misleading

If someone believes they were harmed by Cash App’s “Borrow” loans or repayment practices, they do not need to navigate this alone. A team of lawyers is actively reviewing these issues and exploring arbitration as a way to pursue relief.

To see if they may qualify and to help the investigation move forward, they are invited to complete the existing form on this page.

.svg)